![]() Owner Resource Group is pleased to provide the following wealth management insights from Round Table Wealth Management.

Owner Resource Group is pleased to provide the following wealth management insights from Round Table Wealth Management.

Second Quarter 2021 Review

Dear Clients and Friends,

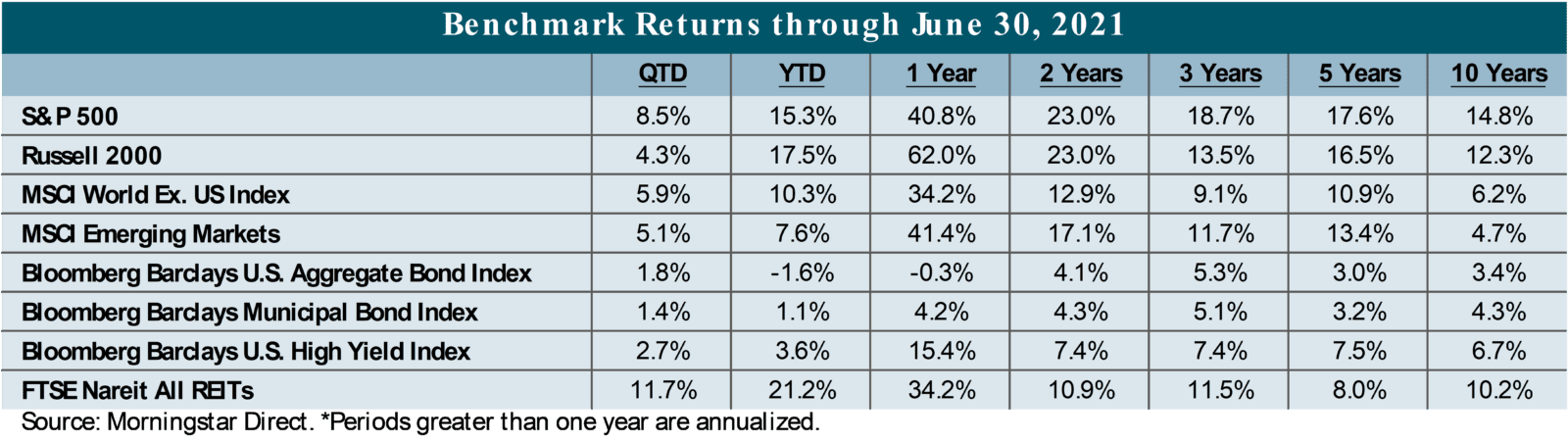

We hope you are enjoying summer! The “dog days of summer” were not discouraging the markets as they continued their upward trajectory with all major equity and fixed income indices generating positive performance for the quarter. As inflation concerns waned, growth equities rebounded and outperformed value-style investments by 6.7% based on Russell 1000 data. The subdued inflation outlook benefited fixed income investors as yields fell and prices increased, allowing the Barclays U.S. Aggregate Bond Index to recoup 1.8% of its negative year-to-date return.

We have not made any material changes to our portfolio positioning since our last correspondence. As we discuss in the Big Picture section below, consumer spending and cash levels (purchasing power), employment opportunities, historically low interest rates and massive government spending all support continued overweight allocations to equities. We recognize risks remain such as mounting U.S. debt, a high probability of tax increases and the COVID-19 Delta variant that is causing concerns outside the U.S.

We welcome a conversation with you to discuss our outlook. If you would like to learn more, please contact us for a personal meeting.

The Big Picture

The U.S. economy continues to expand in the post-pandemic phase. U.S. real gross domestic product increased 6.4% during the first three months of the year and, according to Jerome Powell, Chair of the Federal Reserve, this could reach 7% for all of 2021. [1] Economic forecasters surveyed by the Philadelphia Federal Reserve expect the U.S. economy to increase 7.9% in the third quarter and finish the year up 6.3%. [2] Regardless of the opinion source, nearly all economists and strategists believe the U.S. economy is on an upward trajectory. There are a number of factors driving the robust U.S. economic growth. First, U.S. households remain flush with cash after accumulating approximately $2.6 trillion during the past 18-months. Total money market funds, including institutional accounts, is a whopping $4.6 trillion, all of which earns nearly zero interest income. Additionally, consumer credit card balances are lower than at the start of the pandemic and housing values are up. In fact, the delinquency rate on all credit card loans by commercial banks is at the lowest rate since 1992. [3]

Further to this point, the delinquency rate dropped during this recession, which is the opposite trajectory of credit card delinquencies during the 2001 and 2008 recessions. It is not surprising, therefore, that Consumer Confidence surveys remain high, which supports the expectation that demand for certain goods and services denied during the pandemic may remain at current high levels.

Consumers are very likely to be joined by the U.S. Government in spending large sums. The Biden administration’s desire for significant infrastructure spending gained meaningful support via the public approval by the Problem Solvers Caucus. The group of 29 democrats and 29 republicans announced its bipartisan support for a $1.3 trillion infrastructure plan to be spent over eight years. On a global basis, G7 countries, representing the U.S., Canada, England, France, Germany, Italy and Japan, have formed a positive consensus view of a Build Back Better World Initiative (B3W) that is designed to respond to China’s Belt and Road Initiative, which has been signed onto by over 100 countries. The G7 intent is to narrow the “$40 trillion infrastructure need in the developing world.” [4]

We continue to monitor employment data as an indicator of the U.S. economy’s strength. Unemployment claims continue to soften and the availability of jobs is the highest in recent memory (over 6 million). [5] We suspect that employment data will improve in September, which coincides with a variety of factors including: 1) children returning to full-time, in-person schools, 2) the likelihood of a higher percentage of the population that has received the COVID-19 vaccination, and 3) the termination of enhanced unemployment benefits. In this respect, September could be a behavioral shift in consumer spending as greater presence of in-office workdays could lead to less consumption activity relative to the recent 12 months.

Inflation will likely continue to be on the minds of investors. The on-again and off-again nature of inflation concerns has added volatility to both growth-style equity investments and fixed income markets this year. The latest development came as Jerome Powell expressed his concern that inflation would increase above prior 2021 forecasts and that interest rate increases could occur in 2023 rather than subsequent to that period. While this was a considerable change in communication, the market reaction was muted with the U.S. 10-year Treasury Yield falling about 15 basis points to its current yield of 1.35%. The previously referenced Survey of Professional Forecasters conducted by the Philadelphia Federal Reserve suggests an inflation consensus of 2.2% and 2.3% for 2022 and 2023, respectively.

The flip-side risks of all the spending and available cash highlighted above is a historically high level of U.S. Federal debt, which as of March 31, 2021, was about $28.1 trillion. Certainly COVID-related spending was a key factor in the incremental $6 trillion added during the last 18 months, but the debt has a long history of rising. Since the first quarter of 2001 through the first quarter of 2021, or 20 years, the total U.S. federal debt outstanding has increased approximately 8.2% per year. If this was an investment it would be highly sought after given the S&P 500 averaged approximately 8.8% a year during the same time period. Federal revenues (think taxes collected) were approximately $3.6 trillion in 2020, about $50 billion less than 2019. [6] We bring this data into the conversation because changes to the tax code are highly probable given spending plans and higher interest costs if rates increase. We don’t know what those changes will ultimately resemble, but we would suspect that any material changes will result in market volatility both in equities and taxable fixed income.

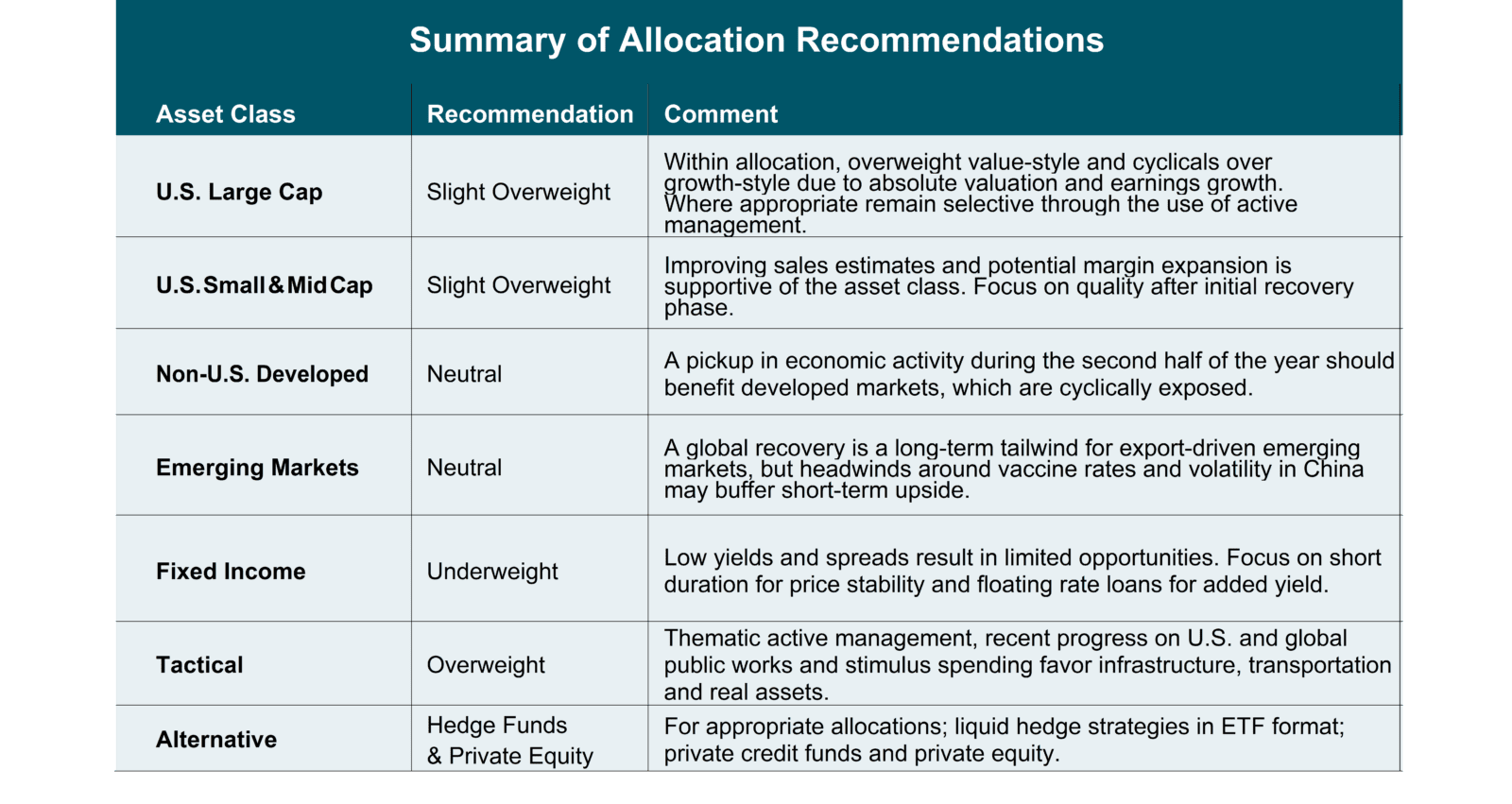

The following summarizes our market outlook. In the near to mid-term, we remain optimistic on U.S. equities and have increasing confidence in developed, non-U.S. equities as the “reopening trade” that has not fully occurred outside of the U.S. and predominately in Europe. We believe the “beta” trade of simply investing in passive indices as part of the U.S. reopening trade is nearing an end, which leaves us to focus on active management that can assemble a higher quality portfolio relative to passive strategies. We are not selling out of passive strategies but complementing those investments with greater active management. Fixed income will remain challenged as the prospect of higher rates and inflation are real, both of which detract from bond prices.

The Outlook

We remain overweight to U.S. large cap equities, with a bias toward value-style and cyclical investments. Analyst expectations project value-style investments, such as the Russell 1000 Value Index, to increase 2022 earnings by approximately 10.1% over 2021 earnings with a forward price-to-earnings of 18.2x. [7] Large cap cyclical companies are projected to grow earnings approximately 22% during the same period and carry only a slightly higher forward P/E valuation of 20.0x. We continue to own growth-style and core passive large cap exposure but have increased exposure to value and cyclicals within large cap allocations.

We reiterate our overweight allocation to the small and mid-cap equity asset class that we initiated last quarter. Supportive fundamentals such as increasing sales growth and depressed margins allow for multiple paths to higher earnings, however, a more selective approach is warranted as we enter the middle stages of the economic cycle. As a result, we have shifted assets from our passive exposure bias held last quarter towards a bias to active managers to capitalize on this more selective approach. We believe the ability of active managers to focus on finding companies exhibiting quality characteristics such as lower debt, higher return on capital and higher margins is a better risk-adjusted approach to this stage of the economic recovery.

We have improved our recommendation within non-U.S. developed markets from an underweight to a neutral weight allocation. Year-to-date, international developed markets have broadly trailed domestic equities due to a slower vaccination rollout and a double-dip economic recession in Europe, which contracted 0.3% in the first quarter compared to 6.4% growth in the United States. Subsequent to the first quarter, many international countries have begun to catch up in vaccination rates, which has coincided with accelerating economic data.

Activity levels in manufacturing and services hit record highs in Europe in the month of June, with expectations that GDP growth will inflect higher in the second half of the year. The pickup in economic activity should continue to support cyclical industries, which are more heavily present in non-U.S. developed equity markets. Whereas the economic growth seems to be priced into U.S. equities, the valuations in non-U.S. developed markets still present a discount, even when adjusted for sector differences. At quarter end, the sector neutral price-to-earnings ratio of the MSCI Eurozone Index was trading at a 10% discount relative to the MSCI USA Index.

On the other hand, we have reduced our overweight allocation to emerging markets to a neutral weight to compensate for our improved outlook in developed markets. While emerging markets still present strong levels of absolute growth, the supply chain constraints globally have tempered some of the short-term expectations in many export-driven EM economies. Additionally, the rollout of the COVID vaccine across emerging markets and Asia has been slower than the developed world. This may impede near-term growth as any outbreaks could deter economic reopening. For instance, in June a COVID outbreak at the Yantian shipping port in China, one of the largest shipping ports in the world, reduced the operating capacity of the port to roughly 30%, creating massive delays in freight transportation globally. We believe emerging markets continue to present an attractive long-term investment opportunity, but the economic recovery in emerging markets will likely continue higher in fits and starts.

We maintain our underweight to fixed income as we enter the third quarter. Yields and spreads remain historically low, resulting in limited opportunities in the asset class. Our allocation remains focused on short-duration investment grade fixed income for price stability, as rate volatility is likely to persist given the recent communication that the Federal Reserve is ready to temper easy monetary policy sooner than previously communicated. We compliment this exposure with below investment grade fixed income to generate additional yield and are comfortable with taking credit risk given the strong domestic economic backdrop.

Tax and Financial Planning News

While the summer months bring relative quiet to Congressional action, we expect some clarity in President Biden’s tax proposals later this fall. For investors who have recognized large capital gains already in 2021, there is still time to do some proactive planning and income tax management. If capital gains no longer receive preferential rate treatment, investors may be served to take action deferring the recognition of gains until a later tax year. By deferring gains past 2024, investors may benefit from a new Congress or President who may have more favorable tax objectives on the horizon. For real estate investors, the 1031 exchange remains a popular mechanism for deferring capital gain recognition as long as the individual takes necessary action in identifying and purchasing a replacement property within the designated time frame. Alternatively, Opportunity Zone investments and funds may be an attractive alternative as capital gain taxes can be deferred into 2026 or later. Traditional income tax management and minimization strategies like charitable gifting, direct indexing, and tax loss harvesting also continue to be opportunities for both recognized and unrecognized portfolio gains. If you have a portfolio with large, embedded capital gains or have experienced a recognition event in 2021, please reach out to a Round Table Wealth Advisor.

[1] Bureau of Economic Analysis; Gross Domestic Product (Third Estimate), GDP by Industry, and Corporate Profits (Revised), 1st Quarter 2021, June 24, 2021.

[2] Federal Reserve Bank of Philadelphia. Second Quarter 2021 Survey of Professional Forecasters.

[3] St. Louis Federal Reserve data through March 31, 2021.

[4] White House press release dated June 12, 2021; FACT SHEET: President Biden and G7 Leaders Launch Build Back Better World (B3W) Partnership.

[5] Bloomberg, L.P.

[6] St. Louis Federal Reserve Economic Data (FRED).

[7] Bloomberg, LP.

*The content herein is provided to you by unaffiliated sources believed to be reliable, but not guaranteed on an as-is basis without any warranties of any kind. In no event shall Owner Resource Group, LLC be liable for any direct, indirect, incidental, punitive, or consequential damages of any kind whatsoever with respect to this content. The content is distributed for informational purposes only and not intended to provide investment advice. The information contained in this article is accurate as of the data submitted, but is subject to change. We strongly recommend you consult your professional business advisors before making any financial or investment decisions.